French markets have discovered some reduction after the primary spherical of its newest election, with shares recovering considerably and bond yields falling after reaching a 12-year excessive. However irrespective of which facet wins in France, the market is afraid that a rise in unsustainable spending could possibly be the widespread denominator.

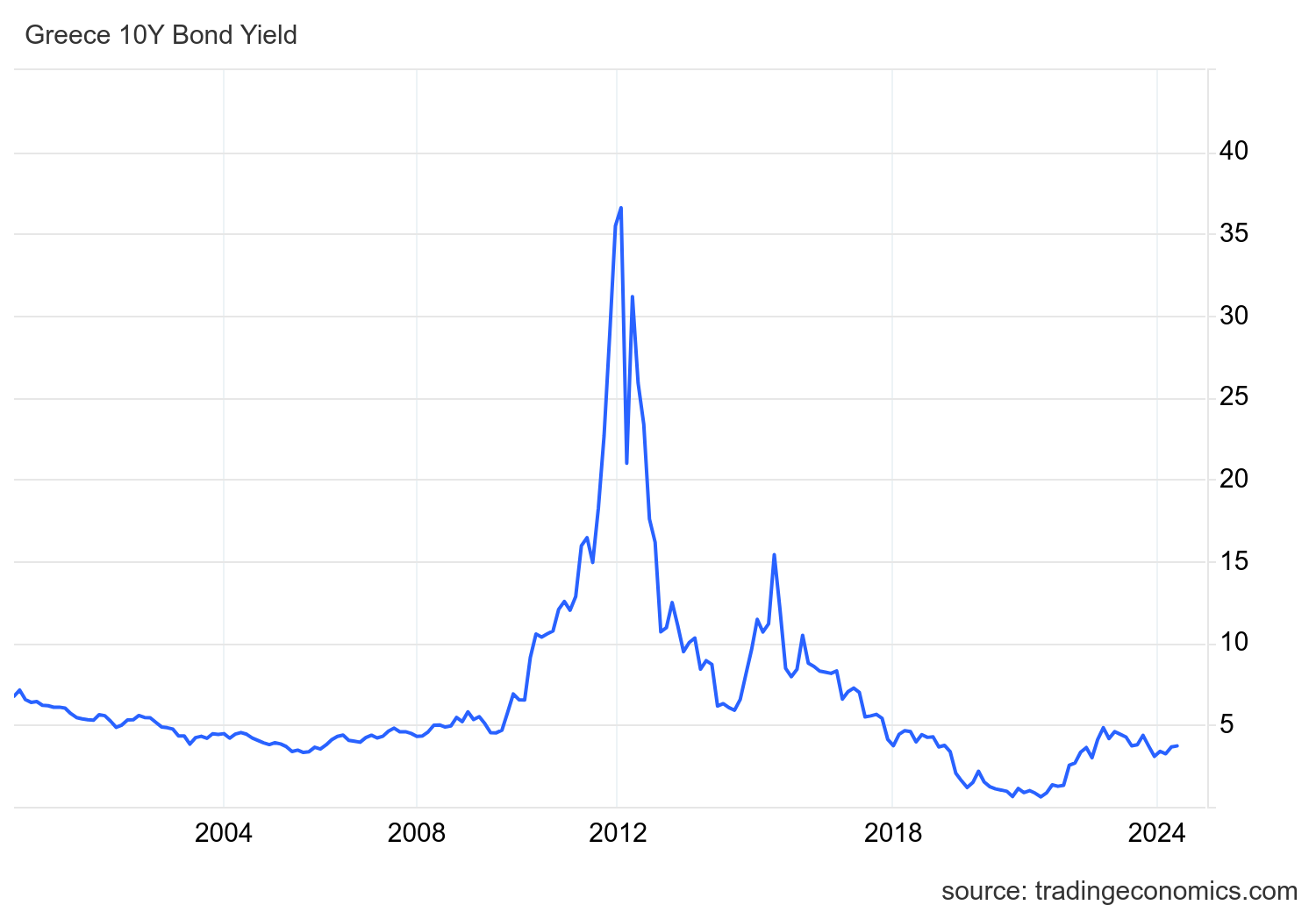

Greece’s sovereign debt disaster after the worldwide 2008 implosion was characterised by an excessively excessive debt-to-GDP ratio, funds deficits, low development, and an over-reliance on revenues from the tourism business. Now, whispers abound within the Eurozone that in France, the same disaster could possibly be on the horizon.

With its entry into the Eurozone, Greece’s central financial institution misplaced a lot of its skill to kick the can down the highway by printing cash. Lengthy and short-term bond yields skyrocketed as the worth of Greek debt plunged and bond buyers fled to greener pastures. Greece’s 2015 default to the IMF totaled €1.6 billion.

France’s debt-to-GDP skyrocketed throughout COVID-19, and after etching downwards, it’s now trending again up and is anticipated to exceed COVID ranges inside just a few years. The French economic system is uncertain of easy methods to react to the coverage guarantees of the left or the proper, so whispers of a possible debt disaster have removed from stopped simply because unstable French markets are experiencing a momentary breath of reduction.

Eyes are on the yield unfold between France and Germany. Yields for “secure haven” German bonds have grow to be the Eurozone benchmark, so the distinction between German yields and people of different international locations has grow to be an indicator of the relative danger tolerance for buyers in European authorities debt. Each France and Belgium have been as soon as thought-about low-risk “core” nations amongst European economies, however that narrative is now altering as the issue of overspending is acknowledged throughout what have been as soon as thought to be economically secure international locations.

In the meantime, the US has most of the identical issues — raging deficits, low development, rising debt-to-GDP ratio, and excessive inflation. The US additionally has extra tips to kick the can down the highway, however few choices for really fixing the issue.

HOW BAD THE US DEBT CRISIS HAS BECOME?

US federal debt hit $34.8 trillion for the first time in historical past

In final 4 years, it has skyrocketed by $11 trillion, an equal of 40% US GDP.

By comparability, reaching the primary $11 trillion it took 220 years.

How does it matter?🧵1/11. pic.twitter.com/TnSUYPvCpd

— World Markets Investor (@GlobalMktObserv) June 26, 2024

In 2010, the IMF outlined an “unsustainable” debt-to-GDP ratio of a complicated economic system to be round 180%. Formally, the present US debt-to-GDP ratio is “solely” about 125%. However together with the Fed itself, World lenders just like the IMF are starting to precise concern about out-of-control funds deficits in main economies.

GDP alone doesn’t inform the story. A big a part of the US GDP whole is based mostly on housing and the over-leveraged actual property market, an financial paper tiger that’s totally depending on low rates of interest and central financial institution cash printing. With actual property taking a variety of 12 to 18% or extra of the GDP pie relying on who you ask, the image isn’t so reassuring. In Greece, the tourism business was too dominant to deal with an financial shock. Within the US, it’s actual property.

There’s additionally the inconvenient fact that prime inflation could make nominal GDP seem increased for the reason that “market worth” of the economic system’s items is increased on paper. When issues price extra it will probably pump the GDP numbers, regardless that market worth alone has nothing to do with whether or not an economic system is wholesome or unhealthy. After all, Keynesians insist that this will equate to “actual” development, and economists proceed debating if excessive GDP fuels excessive inflation, or the opposite means round.

Politicians love spending different folks’s cash as a result of it makes them look good within the quick time period — and all that issues is profitable that subsequent election. However whether or not it’s Greece, France, Japan, or the US, there’s solely a lot debt a rustic can tackle earlier than coming into a black gap. And there’s solely so lengthy that central banks can postpone the inevitable.

Name 1-888-GOLD-160 and communicate with a Treasured Metals Specialist at present!